AI-Native Is a Starting Point, Not a Strategy.

There is a phrase that keeps appearing in African tech commentary right now, and it deserves more scrutiny than it is getting: “AI-native.”

The implication is that being AI-native is the milestone. That building a product on top of large language models, rather than bolting AI onto legacy software, represents a fundamental structural advantage. And in some ways, it does. Tyms AI in Uganda, launching this week with AI agents targeting the operational layer of medium and enterprise businesses, is not retrofitting intelligence onto a spreadsheet workflow. Stub in South Africa is not adding a chatbot to an accounting product that was designed for a desktop in 2009. These are products conceived from the start around what AI can do. That matters.

But AI-native is not the same as Africa-viable. And the ecosystem has not yet fully reckoned with what separates the two.

Alex Okosi, Google’s Africa lead, said it publicly this week in a way that is worth sitting with. Speaking around the latest Google for Startups cohort, he named the structural gap directly: Africa’s AI ecosystem is generating adoption, but not yet generating sustainable, venture-scale businesses. This is not a new observation in private. What changes when Google’s Africa lead says it in public is the political economy of the conversation. Google is not a neutral observer here. It is one of the largest AI infrastructure providers on the planet, and its cloud and API products are part of the cost structure that African startups are building on. When Okosi names the gap, he is also, implicitly, naming a problem that Google has an interest in solving. Or at minimum, in being seen to address.

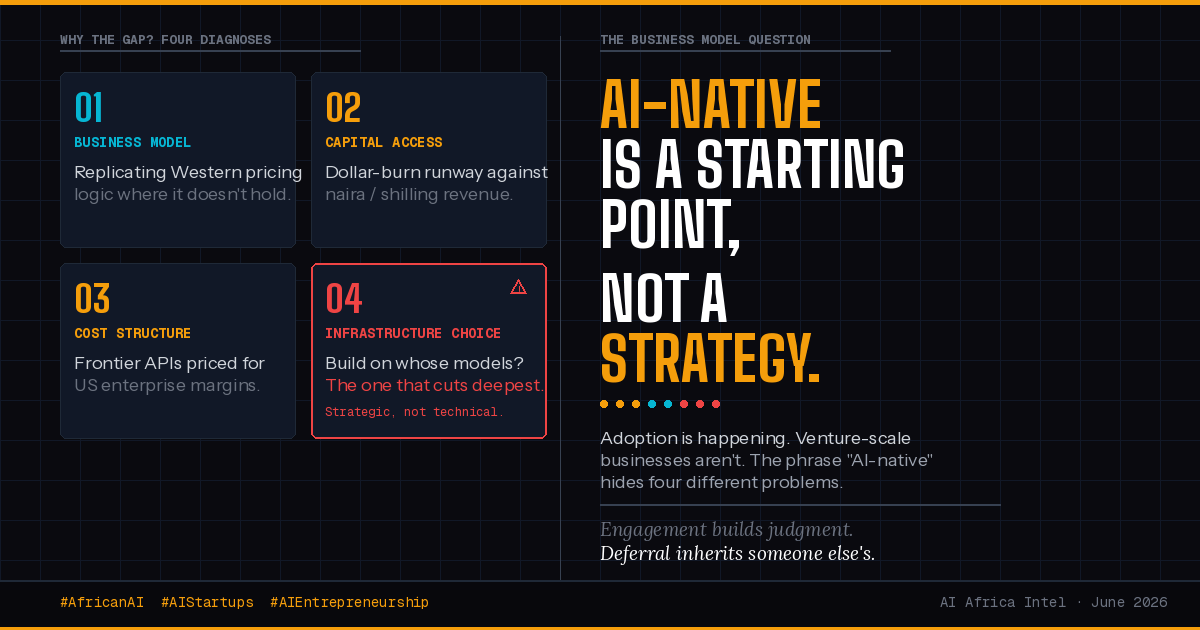

So the diagnosis is useful. But the question it leaves open is the more important one: what is actually causing the gap?

There are at least four possible answers, and they lead to very different prescriptions.

The first is business model design. African AI startups may simply be replicating Western product and pricing logic in markets where that logic does not hold. Stub is going after SME accounting in South Africa, a real and large problem. But QuickBooks and Xero are not standing still. Both are wrapping AI across their existing products, moving down-market, and doing so with distribution networks and brand recognition that a seed-stage startup cannot match on feature parity alone. “AI-native” is not a moat if an incumbent can replicate the feature set within a product cycle. The startups that survive will be the ones that find the angle the incumbents structurally cannot serve, not just the ones that ship first.

The second answer is capital access. African AI startups are raising in an environment where venture investment on the continent fell sharply in 2023 and has not fully recovered. The Flutterwave Series E this week, at a $3.2 billion valuation with Ripple joining the cap table, is the week’s most significant capital signal. But Flutterwave is not a useful comparison for an AI-native startup at seed stage. Flutterwave’s moat was always payments infrastructure built over years across dozens of African markets. The new generation of AI-native companies does not yet have that infrastructure advantage, and the runway math is unforgiving when you are burning dollar-denominated API costs to serve customers paying in naira, shillings, or rand.

The third answer is cost structure, and this is the one the ecosystem is least comfortable naming directly. Frontier AI APIs are priced for US enterprise margins. OpenAI, Anthropic, Google, and their competitors set their pricing against a market where the median enterprise customer has a procurement budget and a tolerance for per-seat or per-token costs that simply does not exist at the African SME level. A product like stub, designed for everyday entrepreneurs, is trying to serve a customer who is price-sensitive in a currency that is not the dollar, using infrastructure that is billed in dollars. That is not a business model problem. It is a structural cost problem. And hoping that API pricing comes down before your runway runs out is not a strategy.

The fourth answer is the one that cuts deepest: that the choice of which AI infrastructure to build on is itself a strategic decision, not just a technical one. Building on frontier API models is fast. It gets you to a demo in weeks. But it creates dependency on pricing, availability, and capability decisions made in San Francisco with no particular regard for what the African market needs or can bear. Building around open-source models, fine-tuned for African languages and use cases, is slower and harder. But it is potentially more defensible, more cost-viable at scale, and more aligned with the longer-term goal of African AI that is actually built for African realities.

This is where the inclusion question becomes structural, not rhetorical. The majority of potential users for products like Tyms AI and stub are not large enterprises with dollar-denominated budgets. They are small business owners, informal sector operators, people running tailoring cooperatives in Kigali or logistics businesses in Accra who need financial and operational tools that work in their language, at their price point, and with their connectivity constraints. If the cost structure of AI-native products keeps them priced for the top of the market, the people with the most to gain from AI-assisted business operations are the ones least likely to access it. That is not an equity footnote. It is a market sizing problem. The addressable market for AI tools in Africa is only as large as the products are accessible.

None of this is a reason for pessimism about what Tyms AI, stub, or the cohort of African AI startups launching right now are trying to do. It is a reason to be precise about what problem they are actually solving, and to stop treating “AI-native” as the answer when it is really the beginning of a harder question.

The African AI startups that build durable businesses in the next three years will not be the ones that moved fastest or raised the most. They will be the ones that solved the cost structure problem honestly, found the customer segment the global incumbents cannot reach, and built something that works at the price points and in the languages of the market they are actually serving.

That is a harder build. It is also the only one that compounds.

What I’m Watching

1. “AI-native” is a starting point, not a strategy — TechCabal →

When Google’s Africa lead Alex Okosi says publicly that the continent’s AI ecosystem is generating adoption but not venture-scale businesses, the useful move is not to debate whether he’s right. It is to ask what the diagnosis implies. The bottleneck is not ambition or technical capability. It is that building on frontier AI APIs denominated in dollars, against customers paying in naira or shillings, produces a cost structure that does not close. Google has an obvious interest in being seen to name this problem. African founders have an obvious interest in solving it before their runway runs out. Those are not the same interest, and the gap between them is where the real strategy conversation needs to happen.

2. The incumbent threat that African AI startups are not talking about loudly enough — Disrupt Africa →

Stub is doing something real: building an AI-native accounting platform for South African SMEs who have been underserved by tools designed for a desktop in 2009. The problem is not the vision. It is the competitive clock. QuickBooks and Xero are not standing still. Both are wrapping AI across their existing products, moving down-market, and doing so with distribution networks that a seed-stage startup cannot match on features alone. “AI-native” is not a moat if an incumbent can replicate the feature set within a product cycle. The African startups that survive this wave will be the ones that find the customer segment the global players structurally cannot reach, not just the ones that ship a cleaner interface first.

3. Flutterwave’s Series E tells you where African fintech is heading, not where it is — Disrupt Africa →

A $3.2 billion valuation and Ripple on the cap table is the week’s loudest capital signal, but the number is less interesting than the composition. Ripple’s participation is not a fintech milestone. It is a statement about where cross-border payment rails are heading: toward blockchain infrastructure, settled outside legacy correspondent banking networks. For African AI startups watching this raise and measuring themselves against it, the more honest read is that Flutterwave’s moat was built over years across dozens of markets, in payments infrastructure that predates the AI moment entirely. That kind of compounding is not available to a company that launched this quarter. The raise is worth noting. It is not a template.

A Reflection

The thing I keep noticing is how often “AI strategy” in African institutions gets framed as a future question.

Not this quarter. Not this cycle. Somewhere past the infrastructure gap, past the regulatory clarity, past the next funding round. A placeholder where a decision should be.

What strikes me is that this framing feels responsible. Measured. It sounds like the kind of caution that protects institutions from expensive mistakes. And sometimes it is exactly that.

But I’ve been sitting with a different read lately. When the dominant lens for a week is deferral, what you’re actually watching is the accumulation of a different kind of risk. Not the risk of moving too fast. The risk of arriving late to a table where the defaults have already been set, the vendors have already been selected, the data architectures have already been built, and the assumptions baked into all of it reflect someone else’s context entirely.

There’s a version of prudence that is genuinely strategic. Wait until the technology matures. Wait until your team has the capacity to govern it. Wait until the regulatory environment is legible. These are real considerations.

And then there’s a version that is just the absence of a decision dressed in the language of strategy.

What I keep returning to is this: the institutions that will shape how AI lands in African markets are not the ones that adopt it last and most carefully. They are the ones that engage now, imperfectly, with enough intentionality to influence what gets built and on whose terms. Engagement is how you develop the judgment to govern. Deferral is how you inherit someone else’s judgment and call it a solution.

The dominant lens this week is deferral. I think the more useful question is what it would take to name that for what it is, in the rooms where it is happening.

One Question

If you are building an AI product for African markets right now, I want to know where the cost structure is actually breaking for you: is it the API pricing, the currency mismatch, or something else entirely that is not in this essay?